If cloud growth in 2020 must be summed up in a single stat, it’s this: Gartner predicts public cloud revenue will grow 6.3% just in 2020 for a total revenue close to $258 billion U.S., up $15 billion from last year. Of course, there is much more nuance in cloud growth.

Tracking cloud growth isn’t easy: does cloud mean the few companies that actually provide and drive the cloud—the private, public, and hybrid cloud providers? Or the thousands more companies that run services on those clouds—the IaaS, SaaS, PaaS, and others?

Luckily, there are a few ways to estimate, measure, and predict cloud growth. In this article, we’ll round up the most important cloud growth storylines in 2020 by looking at:

- As-a-service revenue forecasts and cloud growth

- Positioning and spend among the big cloud providers

- Trends and outlooks

- Cloud use cases

As a service revenue in 2020

“As a service” offerings are the easiest ways for organizations to get involved in the cloud. Software as a service (SaaS) is the most successful of these by far in the first decade of true cloud services. SaaS is all the services and software you run online, trading CapEx license spending for OpEx subscription costs.

But SaaS is not the only player in cloud services. PaaS and IaaS were both big players, and now we’re seeing newer entries, like DaaS.

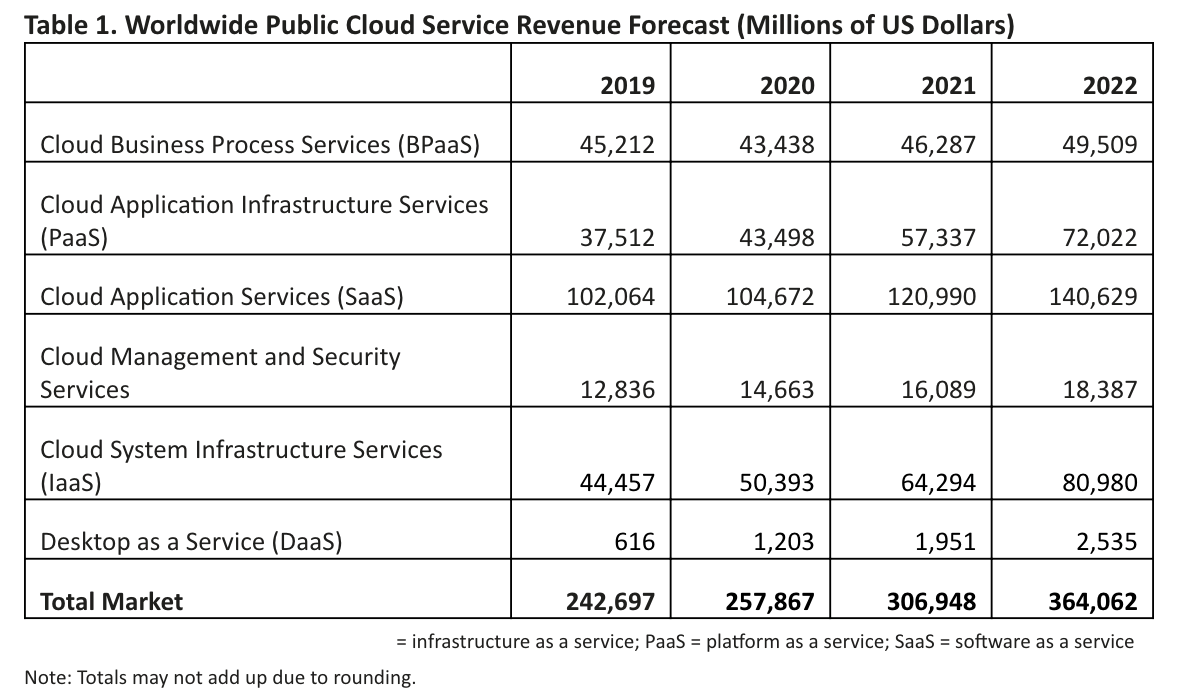

Gartner is a leading technology analyst firm who tracks U.S. and worldwide spending of a variety of technology. This recent chart indicates six leading “as a service” tracks and their forecast revenue. Their most recent research forecasts six key types of cloud services, which we’ll look at in depth below the table:

- BPaaS: Business Process as a Service

- PaaS: Platform as a Service (aka cloud application infrastructure services)

- SaaS: Software as a Service

- Cloud Management and Security Services

- IaaS: Infrastructure as a Service

- DaaS: Desktop as a Service

(Source)

BPaaS: Business Process as a Service

Of the six cloud categories Gartner tracks, BPaaS is one of the smallest players, with its growth barely budging over the next few years, especially relative to the other categories.

This is because a significant proportion of BPaaS customers include SMB organizations with lower requirements on cloud business process services.

PaaS: Platform as a Service (aka cloud application infrastructure services)

The cloud application and infrastructure services will grow experience significant growth between 2020 and 2022, moving up to a solid third place among these six cloud categories. This growth is expected as more organizations migrate their IT workloads to the cloud.

SaaS: Software as a Service

Here is the big growth we expect of the cloud: the public cloud services market will continue to dominate the IT services industry owing to the proliferation of low-cost SaaS solutions that draw workers away from pricey on-prem software licenses.

Gartner predicts that the SaaS cloud application services market will consistently constitute at least one-third of the total public cloud revenue share for the next four years. In 2020 alone, the SaaS market will likely reach over $140 billion in revenue this year.

Cloud Management and Security Services

Cloud management and security services is the next category. Though it’s a smaller player, it’s growth is solid, nearly 50% growth from 2019 to 2022.

IaaS: Infrastructure as a Service

IaaS was one of the original as a service opportunities, but one that didn’t live up to its initial potential. Now, that’s changed. Industry experts see IaaS as the up-and-coming cloud solution that will eventually surpass SaaS in revenue. Gartner clearly agrees with this assessment, estimated IaaS revenue to almost double in four years.

Still, organizations have been slower to adapt IaaS, reportedly due to a skills gap on cloud migration strategies. The sheer quantity of migration strategies that take the past of least resistance—the lift and shift approach—indicate many organizations are ill-staffed to handle modernizing processes, cloud-native development, and refactoring apps that will be so important for true cloud optimization.

DaaS: Desktop as a Service

In terms of raw growth, Gartner predicts DaaS will win out in the next years. This estimate is based on the surge in remote workers, as we noted in our State of ITSM report, which requires secure access to enterprise apps across devices and geographic regions.

Overall Gartner predictions

When it comes to security, Gartner’s forecast highlights the shifting focus toward cloud solutions to run mission-critical security and performance sensitive IT workloads. The cloud industry is proving that on-premise datacenter deployments don’t automatically translate into strong security and that cloud computing is a secure alternative.

Similarly, foregoing some proportion of visibility and control into third-party cloud infrastructure doesn’t compromise the security posture considering the stringent compliance regulations and sophisticated security capabilities designed to protect customer data in the cloud.

For IaaS and PaaS use cases, where organizations are ultimately responsible to manage and secure their own IT workloads, the growth in cloud management and security services market suggests that the industry is responding with effective solutions that help organizations maximize the value potential of their public cloud investments.

This might be the biggest takeaway: The combined market share of IaaS and PaaS revenue will finally surpass the powerful SaaS market revenue.

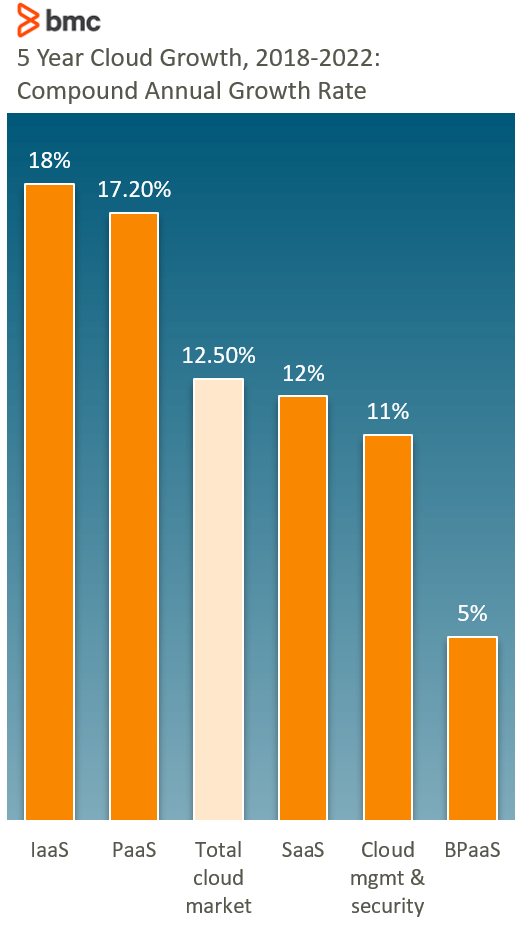

As a service growth rates

Where Gartner looks at revenue, Statista’s latest estimates consider compound annual growth rate (CAGR) worldwide for public cloud services, separated by the same six segments, between 2018 and 2022:

(Source)

Based on Statistica’s information, we can note these trends:

- Like Gartner’s prediction, IaaS and PaaS will combine to finally overtake SaaS in growth.

- SaaS will continue to grow at 12% CAGR, a not insignificant number, that will likely boost this segment well beyond $150 billion revenue in 2020—more than $10 billion more than Gartner predicts.

- More than 60% of surveyed technical professionals from industries around the world stated that their organization was currently running apps using the as-a-service platform Amazon Web Services—which we’ll see more about in the next section.

The Big 3 cloud providers: AWS, Azure & GCP

The next category to look at for cloud growth trends are the cloud providers themselves. The majority of as a service offerings run on someone else’s cloud, no matter if they’re a brand-new startup or a global enterprise.

The hyperscale cloud market segment has largely been dominated by the duopolies of Amazon Web Services and Microsoft Azure. Google Cloud Provider continues to give Azure a run for its 2nd place money, though it did spend less YOY in overall CapEx spending.

Combined, the Big 3 spent $73.5 billion on CapEx in 2019—up seven pecent from 2018. Of course, that isn’t a direct indicator of public cloud spend, but CapEx spending likely contributes significantly to the cost of running hyperscale data centers.

Statista also notes that Microsoft’s intelligent cloud segment, including Azure cloud offerings, has grown rapidly such that its revenue generation now rivals Microsoft’s own, long-established personal computing (PC) segment.

While IBM and Oracle were second-tier players in the public cloud game, their CapEx spending indicates they might be forgoing their spots here in favor of other areas where they can better dominate.

- IBM seems to have pivoted to legacy systems and consulting, with CapEx spending down 36% in 2019.

- Still banking on its database franchise, last year Oracle moved into an app-focused niche on infrastructure strategy.

What’s driving these trends?

Telecommunication companies are refocusing their efforts to capture the IaaS market share based on their dominance in the networking and information communication industry. Open source and containerization technologies are empowering organizations to operate their workloads on public cloud infrastructure at an unprecedented scale by eliminating infrastructure dependencies and application logic.

From a business perspective, organizations are focusing on agility and automation as means to facilitate faster time to value. Organizations are migrating mission critical IT workloads to the cloud to address the business demands of faster compute performance and scalable resources.

Unlike traditional datacenter infrastructure that limits these capabilities, the public cloud model offers the flexibility to scale infrastructure resources on-demand. As a result, public cloud continues to grow in value for SMBs pursuing cloud solutions at an affordable OpEx instead of investing significant CapEx into on-premise infrastructure deployments.

This environment indicates several things for organizations to be on the lookout for:

- Cost optimization remains crucial but elusive. Because IaaS is growing significantly, legacy apps must be optimized to actually achieve cost effectiveness. This means the market for third-party cost optimization solutions and tools will likely expand.

- Greater cloud spend means greater responsibility for CIOs and other management roles to invest wisely. Multi-cloud strategies mean you’ll need to consider provider independence, risk, and vendor lock-in. Specifically, lock-in is expected to decline in the next few years as companies increasingly standup multi-cloud strategies.

- Enterprise agility will increasingly be defined by your in-house cloud talent. How quickly can you stand up the cloud environments you need? For example, securely collaborating across teams and locations.

- Edge technology, including edge AI and edge computing, will become increasingly vital to enterprise success as a result of both increased remote work and security and privacy awareness.

Cloud use cases: public, private & hybrid

Investments in the cloud services segment involve pressing decisions around ROI, security and innovation potential to transform businesses. Various cloud service models offer unique tradeoffs and value propositions for different use cases:

- Public cloud offers cost advantages through sharing of cloud infrastructure resources between multiple tenants at an acceptable security and availability Service Level Agreement (SLA).

- Private cloud offers strong security and availability as the infrastructure is isolated between the users and the resources are dedicated to individual organizations.

- Hybrid cloud offers a mix of public and private cloud deployments optimized for cost, security, and performance based on what your organization needs.

The hybrid cloud market will experience rapid growth, with 90% of organizations investing in the technology by 2020. The private cloud infrastructure market will grow at a slower rate than the public cloud services market according to IDC but will continue to gain importance in IT investment decisions as organizations pursue secure and reliable alternatives to on-site datacenter deployments.

Cloud outlook: full speed ahead

The proliferation of public cloud solutions is driving business transformation toward agility in the world of growing uncertainties, hyper growth, and rapidly changing market trends. Businesses need to analyze, understand, and proactively adapt business services faster than ever before.

Like any technology, there’s been ongoing healthy debate about the public cloud’s actual usefulness—beyond its smart marketing. That debate is likely paused, at least for the foreseeable future of remote work. As cloud grows, we’ll also rely on other tools for remote work such as:

- Secure collaboration software

- Mobile device management

- Security

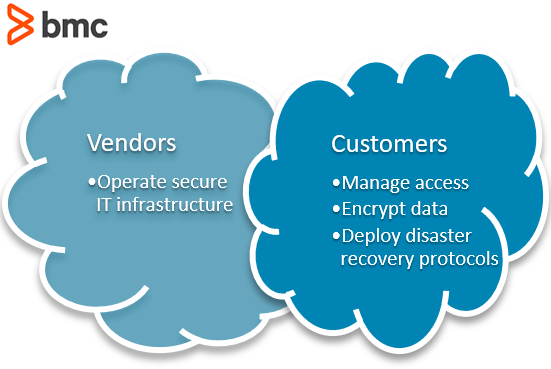

Shared model of responsibility in many cloud environments

The prevalence of public cloud solutions represents opportunities for organizations of all sizes and industry verticals to disrupt their respective industries. The technology allows more startups and SMB firms to compete in innovation against their larger counterparts, allowing them to focus on their core business offerings, without having to invest significant resources or time to scale the underlying technology infrastructure.

Businesses are recognizing the value of public cloud solutions as they accelerate their digital transformation and follow evolving customer roadmaps. The need for elastic, scalable, and low-cost cloud options will continue to increase as along with security and performance requirements. Future public cloud offerings will be more secure, reliable, and vertical-specific to facilitate profitable and agile digital transformation, especially in these key areas:

- Application and data platforms

- Distributed app workloads

- DevOps-driven SLDC practices

Consequently, the growth trajectory of public cloud services market revenue will remain consistent as organizations continue to embrace SaaS and IaaS solutions to power their businesses.

Additional resources

For more on this topic, explore the BMC Multi-Cloud Blog and these articles: